Soft US services and job surveys support rate cut expectations for later in the year. Australia’s headline growth falls in Q1, and South Korea’s currency and stock market get a boost from an election ending months of uncertainty.

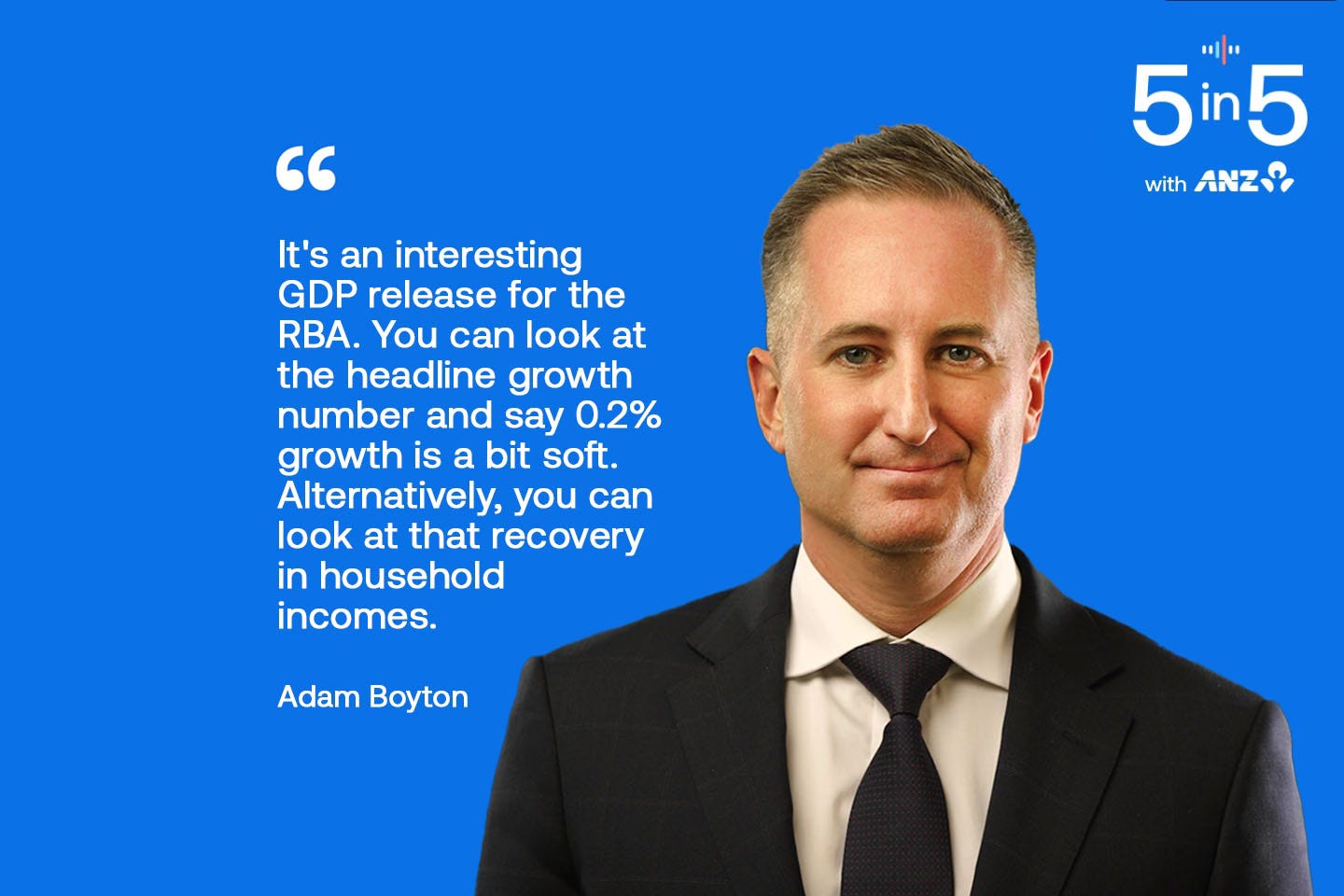

In our deep dive interview, ANZ Head of Australian Economics Adam Boyton explains why the economy is in better shape than yesterday’s Q1 GDP indicated.

5 things to know in 5 minutes:

US Treasury yields fell this morning on growing expectations the US Fed could make two rate cuts later this year. ADP jobs growth came in well below expectations, while the ISM services index showed activity unexpectedly contracted in May. ANZ Economist Bansi Madhavani says Friday’s payrolls report will be crucial for the Federal Reserve’s rate cut determinations.

The European Central Bank has a rate call tonight after annual inflation fell below its 2% target yesterday. Bansi says while new PMI data shows some signs of recovery, ongoing tariff headwinds pose a risk to growth.

Australia’s economy grew 0.2% in Q1, in line with ANZ Research’s final forecast. But it was below the 0.6% in December, and a market expectation for 0.4%, due to weaker public demand. ANZ Head of Australian Economics Adam Boyton says the economy isn’t as weak as the headline suggests.

South Korea’s annual CPI inflation fell slightly to 1.9% in May - just below the central bank’s 2% target. ANZ Economist Krystal Tan says there’s room for another 25 basis point rate cut.

Meanwhile, the South Korean won, and its stock market rose yesterday following the election of a new President, ending months of political uncertainty that had weighed on economic activity and the currency. Krystal says all eyes are now on trade talks with the United States.

Cheers,

Alex (standing in for Bernard).

PS: Catch you tomorrow with analysis of the ECB’s rate decision.