Markets start the week off the back of concerns on Friday that the US Fed might delay rate cuts after June’s stronger PMI. All eyes are on US PCE data this Friday, and the Yen starts the week on the back foot.

In our bonus deep dive interview, ANZ Senior China Strategist Zhoapeng Xing analyses significant changes on the way for China’s monetary policy regime.

5 things to know:

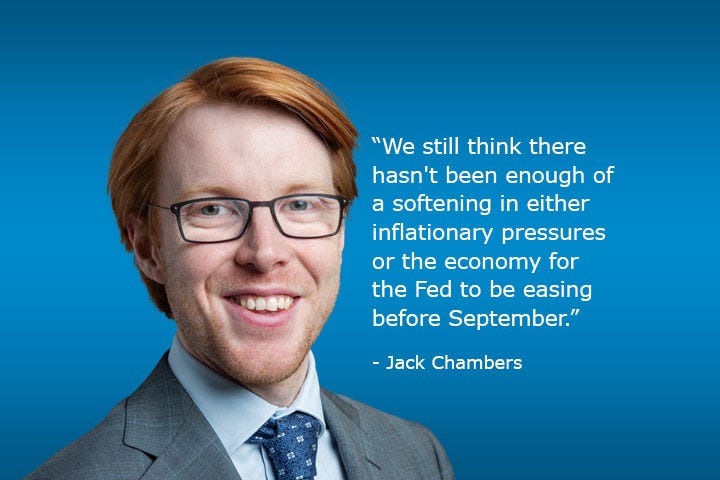

Global markets start the week with concerns around delays to the Fed’s rate cut timing, after PMI data showed activity in the US expanded at a faster rate in June. All eyes this week will be on Friday’s core PCE inflation data. ANZ Senior Rates Strategist Jack Chambers says monthly core PCE is expected grow 0.1% in May, which would be the lowest this year.

Europe’s PMI showed softer-than-expected growth, with contraction in France linked to the upcoming snap election there. ANZ FX Analyst Felix Ryan says political uncertainty has been a driver for the Swiss Franc rising in recent weeks, ahead of Friday’s surprise interest rate cut by the Swiss National Bank.

In Australia, the focus this week is the May CPI indicator on Wednesday. Jack says it’s expected to tick up slightly to 3.8% annually.

Japan’s annual CPI rose slightly to 2.8% in May, a touch below forecast. That was led by strength in energy and goods prices while the services contribution was steady. Felix says that, while the headline measure rose, core measures did throw up some questions for how the Bank of Japan might read the data.

The Yen slumped further on Friday - with the US dollar rising to 159 against the weaker Japanese currency. Jack says that’s partly due to the Bank of Japan delaying its decision on when to begin quantitative tightening.

Cheers

Alex (standing in for Bernard, who’s on a mid-winter break)

PS: Catch you tomorrow with a look at how the RBA’s hawkish turn last week contrasted with dovishness elsewhere.