Global PMI surveys suggest the US economy is rollicking along in a way that might force the Fed to keep rates high for even longer. New Zealand retail sales bounce and there’s hope tax cuts in next week’s Budget might give them more of a boost.

In our bonus deep dive interview, ANZ Senior International Economist Tom Kenny reviews how the Bank of Japan’s commentary has shifted in recent months, and why that points to more rate hikes.

5 things to know:

US bond yields rose 4-5 basis points and US stocks fell half a percent overnight after PMI surveys were stronger than expected. ANZ Head of G3 Economics Brian Martin says markets saw the figures as meaning the Fed would hold rates high for even longer on a ‘no landing’ scenario for the US economy.

Japan’s nationwide CPI data for April is due later today. ANZ Senior International Economist Tom Kenny says the market expects the annual rate to ease from 2.7% to 2.4%.

The Bank of Korea held its policy rate at 3.5% yesterday and reiterated it wanted to maintain restrictive policy. But ANZ Economist Krystal Tan says it has left the door open to rate cuts in the second half of the year.

Singapore’s final Q1 GDP was unchanged at 2.7% annual growth and core CPI was steady at 3.1%. ANZ Head of Asia Research Khoon Goh says elevated core inflation points to monetary easing being a 2025 story.

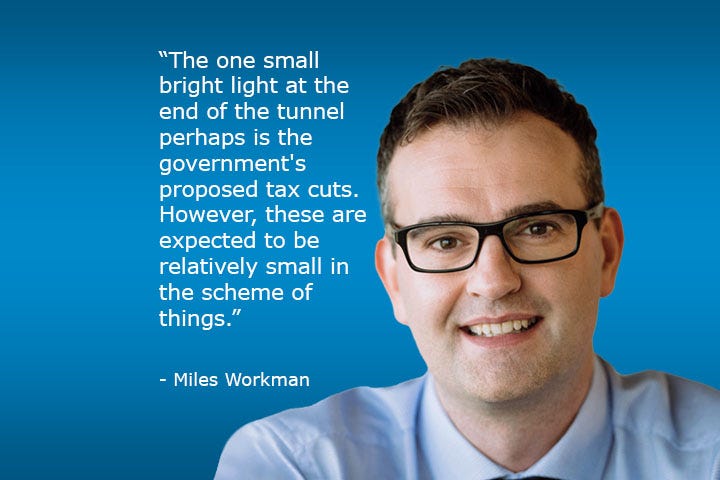

New Zealand retail sales rose 0.5% in Q1, following eight quarterly falls. ANZ Senior Economist Miles Workman says the bounce presents some upside risk to the RBNZ’s Q1 GDP forecast, but the economy remains soft.

Cheers

Bernard

PS: Catch you next week with details from Japan’s CPI today and previews of Australian inflation data due next Wednesday and New Zealand’s budget on Thursday.